The Best Credit Cards in Japan for Unlocking Rewards

Make your wallet work smarter in Japan by choosing the credit card that will gain you the most cash-back point incentives.

Read on for a list of the major credit card companies and their various pros and cons for expats in Japan, and a snapshot of the ideal persona for each option.

Rakuten Card—best for earning extra points

According to various surveys of netizens in Japan, the Rakuten card is one of the most used credit cards in Japan. It’s also one of the easiest for foreigners in Japan to receive.

Pros

1% cashback points (¥100 = 1 point);

Points can be used at a vast number of stores throughout Japan

No annual fees for their regular card

Contactless checkout payments with Visa touch

Free travel insurance plan

Initial credit card limit: ¥700,000 to ¥1,000,000

Credit card types available: VISA, Mastercard, JCB, American Express

Additional credit card services: Family card

During campaign seasons, if you sign up for their credit card and mobile phone plan or bank account at the same time as the credit card, you get a bonus of between ¥5,000 to ¥30,000 cashback points.

Cons

If you're more of an Amazon shopper, then the Amazon or JCB cards will earn you more points.

If you want the ETC tie-in (highway card), that will cost you ¥550 per year on the regular card. (The ETC tie-in is free if you're on the Rakuten Gold or Premium card.)

Anyone who spends more than ¥9,000 per month on Rakuten’s ecommerce site should use the Rakuten Gold card for higher points.

Ideal for: Anyone using one or more of Rakuten's services (phone, bank, utilities, NISA, etc.). The cashback system for purchases made on the Rakuten store increases with the number of Rakuten services you use (up to 12x).

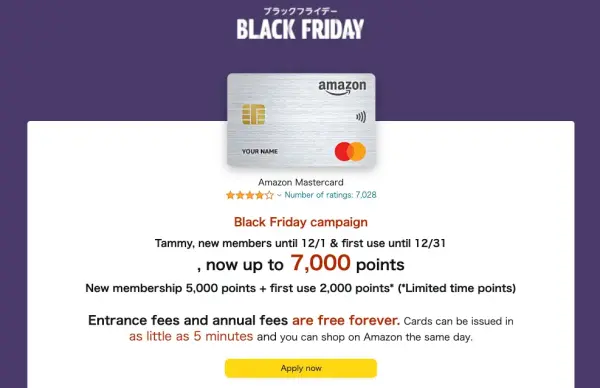

Amazon card—best for Amazon shoppers

The Amazon credit card is noted by some in the expat community as an easy-to-obtain credit card. However, be warned: the application process might take a month and a half.

Pros

No annual fee

1% cashback points (¥100 = 1 point)

1.5% cashback points when shopping on Amazon; 2% cashback points if you're a Prime Member shopping on Amazon

1.5% points if you use your Amazon card at 7-eleven, Lawson, or Family Mart

Signup campaign points: ¥2,000 to ¥5,000, depending on the campaign season

Initial credit card limit: Decided on a case-by-case basis

Credit card types available: Mastercard

Additional credit card services: ETC tie-in is free

Cons

Fewer options for where to spend points when compared to Rakuten

The credit card application process can take up to 6 weeks

Does not offer VISA or JCB

Ideal for: Anyone who is a heavy Amazon shopper.

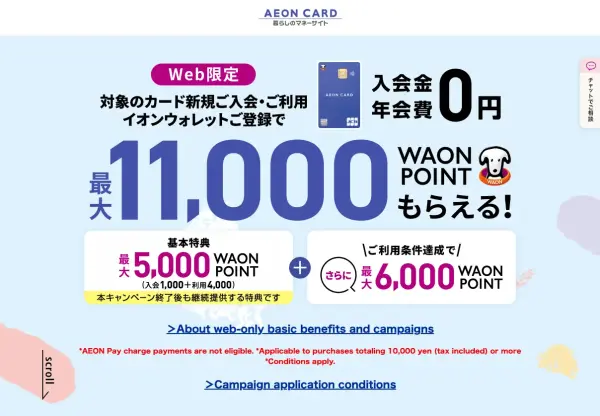

Aeon Card Select—An all-in-one credit and bank card

The Aeon Card Select is an excellent option for anyone who lives near any of Aeon’s big chain stores and frequently shops there. It’s also an easy card to apply for if you do so in person at a mall counter.

Pros

No annual fee

¥200 = 2 points at Aeon-affiliated stores (Aeon malls, Max Value, The Big, etc.)

¥200 = 2 points on Aeon Card W point days (10th of each month)

¥300 off for Aeon Cinema tickets if you reserve online and then pay with your Aeon credit card

Easy for foreigners to apply to if you apply in person at an Aeon mall when they are doing a signup campaign

Signup campaign points: ¥6,000 to ¥11,000, depending on the campaign season

Can get an invite for a free Aeon Gold credit card

All-in-one: Credit card, debit card, and Waon point card

Credit card limit: ¥100,000 to ¥1,000,000 per month

Credit card types available: Visa, Mastercard, JCB

Additional credit card services: Free ETC card tie-in

Cons

0.5% cashback points for shopping at non-affiliated stores; which is less than Rakuten

No travel insurance connected to the credit card

Must open a bank account at the same time

If you don't go to a counter, you'll need to apply via an online form and be familiar with typing in Japanese

Ideal for: Anyone who shops at Aeon frequently or who wants to save Waon points or create an Aeon bank account.

Mitsui Sumitomo (NL)—best card for convenience store users

The Mitsui Sumitomo card is touted as a strong option if you’re concerned about security. There’s no number printed on the card, and it uses the one-touch contactless technology for payments.

Pros

No annual fee

7% percent cashback points at Mcdonald's and participating convenience stores when using contactless payment

Numberless credit card makes losing the credit card less of a worry

Can also be connected to Apple Pay for mobile payments

If you spend ¥1,000,000 or more in a year, you may receive an invitation to apply for the Mitsui Sumitomo Gold (NL) card (subject to approval) with the annual fee (normally ¥5,500) waived permanently from the second year onward.

Signup campaign points: ¥6,000

Credit card limit: ¥1,000,000

Credit card types available: Visa, Mastercard

Additional credit card services: free enrollment in travel insurance

Cons

0.5% cashback for regular shopping at non-participating stores

Must use an app to check statements and confirm personal information

Ideal for: Anyone who frequents convenience stores, McDonald's, Mos Burger, Saizeriya, Gusto, Bamiyan, Coco's, Sukiya, Doutor, Jonathans, Excelsior Caffe, etc.

EPOS card—easiest starter credit card

The EPOS card is another easy-to-apply for credit card if you do so in person at a Marui mall counter during a campaign season. It’s often considered a starter card in Japan and is used by many students and homemakers.

Pros

No annual fee

0.5% to 1.25% cashback points per ¥100

Touted as an easy-to-get Japanese credit card that even students and homemakers can get

Easy for foreigners to apply for if you apply in person at a Marui mall when they are doing a signup campaign

If you spend more than ¥500,000 in a year, you get a free invite to the EPOS Gold credit card

10% off at Marui during their 4x yearly sales

Signup campaign points: ¥2,000

Initial credit card limit: ¥100,000 to ¥300,000

Credit card types available: Visa

Cons

Cashback points at non-participating stores is 0.5%

No travel insurance connected to the credit card

Ideal for: The EPOS card is an easy-to-get starter card for students, homemakers, and those who want an easy path to a Gold credit card.

JCB CARD W—smart choice for spenders

The JCB Card W is the smartest choice for young adults looking to maximize their rewards. This card offers all its benefits if you sign up between the ages of 18 and 39. Plus, you’ll keep all the benefits when you reach that age.

They have a sign-up campaign where you can earn up to 20,000 yen cashback.

Pros

No annual fee for those under 39; continuous benefits after surpassing the sign-up age

1% cash back on all purchases

Up to 5.5% rewards for partner stores like Amazon, 7-Eleven, and Starbucks

Up to 10.5% rewards during special campaign seasons.

Receive real-time spending notification

Credit Card Types Available: JCB only

Additional card services: numberless card option and overseas travel accident insurance

Cons

Only available for applicants aged 39 and under (18–39). Those who are already 40 cannot apply.

High cashback for specific stores and during specific times of the year

Ideal for: Those who spend primarily in Japan or travel frequently within Asia, and who can benefit from high cashback rates without worrying about annual fees.

Summary table of the best credit cards in Japan

Here, we summarize the best credit cards for foreigners to apply to.

Credit Card |

Cashback and Points |

Special Features |

Ideal For |

Rakuten Card |

・1% cashback (¥100 = 1 point) ・Up to 12x points with Rakuten services |

・Contactless payments ・Free travel insurance ・Family card option ・Bonus cashback during campaigns |

Users of Rakuten's services and frequent Rakuten shoppers |

Amazon Card |

・1% cashback ・1.5% at convenience stores ・2% for Prime members on Amazon |

・ETC tie-in free ・Targeted benefits for Amazon purchases |

Heavy Amazon shoppers |

Aeon Card Select |

・2 points per ¥200 at Aeon stores ・0.5% elsewhere |

・All-in-one credit and Waon point card ・Discounts at Aeon Cinema |

・Frequent shoppers at Aeon stores ・Those wanting an integrated bank and credit card |

Mitsui Sumitomo (NL) |

・7% at McDonald's and certain convenience stores ・ 0.5% elsewhere |

・Numberless card ・Free travel insurance ・Automatic upgrade to Gold card on high spend |

・Convenience store frequenters ・Those concerned with security ・Great cashless payments interface |

EPOS Card |

・0.5% to 1.25% per ¥100 |

・10% off at Marui ・Invites to EPOS Gold with higher spend |

・Students, homemakers, first-time credit card users |

JCB Card W |

・1% on all purchases ・Up to 5.5% at partner stores ・Up to 10.5% during campaigns |

・Numberless card option ・Real-time spending notifications ・Overseas travel accident insurance |

・Applicants aged 18-39 ・High spenders at partner locations |

Foreigner credit card application tips

As a foreigner in Japan, getting rejected for bank accounts and credit cards is common.

But here are some times I’ve picked up and seen while living in Japan.

Apply for a credit card in person: Places such as a Marui/Kitte department store or the Aeon mall have staff who will help you with the application process, and you can get the card on the same day.

Consider department store and supermarket credit cards: These are often the easiest to obtain. Places like Marui offer the EPOS card, and Aeon Mall offers the Aeon card, which is quite lenient towards applicants.

Use your current bank account relationship: if you already have a bank account with SMBC, you can apply for their Mitsui Sumitomo credit card.

Initial acceptance to get more cards: Once you have your first credit card and a few months of credit history, you can apply for more cards much more easily.

Credit cards and cash withdrawals in Japan

In general, you can use your Japanese credit card to withdraw cash, although the particulars will depend on the specific card you have.

Credit Card |

Cash Withdrawal in Japan |

Cash Withdrawal Overseas |

Notes |

Rakuten Card |

✅ Yes |

✅ Yes |

Cashing limit required |

Amazon Card (SMBC) |

✅ Yes |

✅ Yes |

Setup via Vpass app |

EPOS Card |

✅ Yes |

❓ Not clearly stated |

Strong domestic support |

Mitsui Sumitomo NL |

❌ Not confirmed |

❌ Not confirmed |

No official info found |

Aeon Card Select |

❌ Not confirmed |

❌ Not confirmed |

Focused on Waon/AEON integration |

JCB Card W |

❌ Not confirmed |

❌ Not confirmed |

Focused on shopping/insurance |

How to optimize credit card spending in Japan

The secret to maximizing credit card rewards is knowing where each card shines and planning your spending accordingly. The Rakuten Card gets ridiculously good when you use multiple Rakuten services—phone, internet, shopping, banking. Stack enough services and you can hit 10-12% back on Rakuten purchases, which is insane by any standard.

Seasonal bonuses are where the real money is, but you need to pay attention. JCB Card W runs campaigns all the time, sometimes doubling or tripling points at specific stores. Time a big purchase right and you can earn months' worth of regular rewards in one go. The key is actually reading those promotional emails instead of deleting them.

Don't sleep on utility bills—it's free money sitting there every month. Most utilities accept credit cards now, and while some charge processing fees, the math usually works out in your favor. Set up autopay for electricity, gas, water, and internet, and you'll earn points without thinking about it.

Card Type |

Best For |

Avoid For |

Pro Tip |

Rakuten Card |

Rakuten online shopping and ecosystem purchases |

Non-Rakuten shopping |

Stack services for massive multipliers |

Amazon Card |

Amazon + convenience stores |

Everything else |

Prime membership boosts Amazon rewards |

JCB Card W |

Partner stores + campaigns |

Regular purchases |

Watch for limited-time bonuses |

Mitsui Sumitomo |

McDonald's + conbini |

Department stores |

Use contactless for 7% back |

A typical expat spending ¥200,000 monthly might earn ¥2,000-2,400 yearly with a Rakuten Card, while the same spending could yield ¥2,000-3,000 with an Amazon Card depending on where you shop. These numbers assume you're not gaming the system or hitting special categories.

The Mitsui Sumitomo Card can be a goldmine if you eat at McDonald's and shop at convenience stores regularly. That 7% back adds up fast—someone spending ¥50,000 monthly at participating stores could earn ¥42,000 annually. But if you don't fit that spending pattern, you'll barely earn anything.

Annual Spending |

Rakuten Earnings |

Amazon Earnings |

JCB W Earnings |

Mitsui Sumitomo Earnings |

¥1.2M |

¥12,000 |

¥12,000-18,000 |

¥12,000-30,000 |

¥6,000-84,000 |

¥2.4M |

¥24,000 |

¥24,000-36,000 |

¥24,000-60,000 |

¥12,000-168,000 |

¥3.6M |

¥36,000 |

¥36,000-54,000 |

¥36,000-90,000 |

¥18,000-252,000 |

Annual fees kill returns fast. The Rakuten Gold Card needs ¥200,000 in Rakuten shopping just to break even on its ¥2,200 fee. Premium cards often require spending levels that most people never reach. Be honest about your spending patterns before paying annual fees.

Credit cards in Japan that include travel insurance

One major perk of certain Japanese credit cards is complimentary travel insurance. While coverage varies depending on the card, it can provide valuable peace of mind when you're traveling abroad—or even domestically in some cases.

Most credit cards that include travel insurance fall under two categories:

利用付帯 (riyō futai) — Coverage only applies if you use the card to pay for travel-related expenses (e.g., plane tickets, hotel bookings).

自動付帯 (jidō futai) — Coverage applies automatically, regardless of how you paid for your trip (common with gold or premium cards).

Here’s a breakdown of the major cards offering travel insurance benefits:

Card Name |

Insurance Type |

Coverage Style |

Max Coverage |

Rakuten Card |

Overseas travel |

利用付帯 |

Up to ¥20 million |

EPOS Card |

Overseas travel |

自動/利用付帯 |

¥500K–¥20 million |

JCB CARD W |

Overseas + shopping |

利用付帯 |

Up to ¥20 million |

Mitsui Sumitomo (NL / Gold) |

Overseas & domestic travel |

自動/利用付帯 |

Up to ¥30 million |

Aeon Gold Card (Invite-only) |

Overseas + domestic travel |

自動付帯 |

Up to ¥50 million |

Amazon Mastercard |

Overseas travel |

利用付帯 |

Up to ¥2 million |

💡 Note: The regular Aeon Card Select does not include travel insurance, but the Aeon Gold Card (available by invitation) does.

For frequent travelers, especially those flying internationally, choosing a card with built-in travel insurance can reduce the need to purchase separate policies. Just make sure to review each card’s policy details and confirm whether the coverage is automatic or requires using the card for travel purchases.

What to know about credit score building in Japan

Japan's credit system is nothing like what you're used to back home. There's no single credit score that follows you around—instead, each bank keeps its own records and makes decisions based on their internal systems.

The main credit bureaus, JICC and CIC, exist but don't share information the way Experian or Equifax do. Essentially, your good credit score from overseas means absolutely nothing here.

Building credit in Japan takes time and patience. Most financial institutions want to see at least six months of perfect payment history before they'll even consider raising your credit limit or offering you better products. Don't expect much at first—most foreigners start with limits between ¥100,000 and ¥300,000, regardless of their income or positive credit history. It's frustrating, but that's just how conservative Japanese banks are.

The good news is that after about a year of consistent payments, doors start opening. Japanese banks love "relationship banking"—the more products you have with them (savings account, salary deposit, insurance), the better they treat you. This is why many expats find success by consolidating their banking with one institution rather than shopping around for the best rates.

How to pay your credit card bill in Japan

Paying your credit card bill in Japan is more straightforward than getting approved for the card in the first place, but there are some quirks you need to know about.

Most Japanese credit cards use automatic bank withdrawals as the default payment method, which means you'll set up a direct debit from your Japanese bank account when you apply. This happens on a specific date each month—usually the 27th—and if there's not enough money in your account, you'll get hit with late fees and potentially damage your credit standing.

The automatic withdrawal system works well once you get used to it, but it can catch newcomers off guard. Unlike credit cards in other countries where you might pay online, send a check, or use cash payments, Japanese cards expect you to maintain sufficient funds in your designated bank account.

You'll typically get your statement about a week before the withdrawal date, giving you time to transfer money if needed. Most cards send statements both physically and electronically, though navigating the online portals in Japanese can be challenging initially.

If automatic withdrawal fails or you want to make additional payments, you have several options. Most convenience stores accept credit card payments at their ATMs or service counters—just bring your statement and cash. Online banking through credit card issuer's website or app is becoming more common, though English support varies.

Some cards also accept payments through bank transfers, but you'll need to use the specific account numbers and reference codes provided by your card company.

Understanding revolving payments and interest rates in Japan

Revolving payments (リボ払い) in Japan work differently than you might expect, and honestly, they're usually a bad deal.

Unlike other countries where you can choose to pay a minimum amount each month, Japanese revolving payments typically involve paying a fixed amount regardless of your balance. So if you set up ¥10,000 monthly payments and charge ¥50,000, you'll be paying that same ¥10,000 every month until the balance is cleared—plus interest that can reach 15-18% annually.

The sneaky part is how aggressively Japanese card companies push revolving payments. They'll offer promotional campaigns with bonus points if you sign up for revolving, or they'll make it the default option during card applications.

Some cards even automatically convert large purchases to revolving payments unless you specifically opt out. The Rakuten Card is notorious for this—they'll send you offers to convert purchases to revolving with "convenient low monthly payments" that end up costing you hundreds or thousands of yen in interest.

Most financial advisors recommend avoiding revolving payments entirely unless you're facing a genuine emergency. The interest rates are high, the payment structure is inflexible, and it's easy to lose track of how much you're actually paying.

If you do find yourself in revolving debt, you can usually pay it off early through online banking or by calling customer service. Just make sure you understand the payoff process—some cards make it unnecessarily complicated to discourage early payment.

Frequently asked questions

What are the eligibility requirements for Japanese credit cards?

To be eligible for a Japanese credit card, you must be on a valid non-tourist visa and provide a bank account and valid ID (passport, My Number card, driver's license, residence card, health insurance card, etc.). Some banks may also ask you for your inkan (personal seal) and a tax slip showing your previous year's income.

Which is the easiest credit card for foreigners to get in Japan?

The easiest credit cards for foreigners to get in Japan are the Rakuten credit card and the Amazon credit card for those applying online. For those applying in person at a counter, the Aeon credit card and the EPOS credit card are reputed to be easy to apply for, as the staff will help you enter your middle name in the credit card application.

What are some tips for getting a credit card in Japan?

One of the most-touted tips for getting a credit card in Japan is to apply at a mall counter and fill out a paper-based credit card application. The staff will help you enter your middle name correctly into their system, which is often a sticking point for foreigners applying online. And they will also walk you through all the other information you will need to provide. Other tips to keep in mind: Avoid asking for "キャッシング機能" as this is sometimes a red flag and could prevent you from being issued a credit card. Also, if you fail an application, wait 6 months before applying. This way, credit card screening about the failed application won't be available for the next credit card company to access.

Do Japanese credit cards work abroad?

Yes, as long as it’s a global brand (Visa, Mastercard, AmEx, JCB). Make sure you enable international usage and check foreign transaction fees (typically 1.6%–2.2%).

Can I link my card to mobile payments like Apple Pay or Google Pay?

Yes, many cards like Mitsui Sumitomo (NL), Rakuten, and EPOS support Apple Pay and Google Pay. However, compatibility depends on your phone model and the card brand (Visa/Mastercard/JCB).

What happens if I lose my card?

Most issuers allow you to freeze or cancel your card via app or phone support. Numberless cards like Mitsui Sumitomo NL or JCB CARD W offer added security if your physical card is lost.

Can I increase my credit limit later?

Yes, most issuers allow limit increases after 6–12 months of on-time payments. Some may request proof of income again.

In closing

The best Japanese credit card is one that aligns with your personal spending habits, lifestyle, and financial goals.

Whether it's the Rakuten Card for those who plan to use the Rakuten ecosystem, the Amazon Card for frequent Amazon shoppers, or the Aeon Card Select for Aeon loyalists, each card has unique benefits tailored to different needs.

Understanding the pros and cons, eligibility requirements, and application tips for each option ensures you will make an informed choice.

Spending too long figuring out your Japanese mail?

Virtual mail + translation services start at 3800 per month. 30-day money-back guarantee.