Why Japan's Fiscal Year Starts in April and What It Means for Foreign Business Owners

Japan's fiscal year (会計年度, kaikei nendo) runs from April 1 to March 31.

Unlike most countries that operate on a January-to-December financial calendar, Japan resets its government budgets, corporate accounting cycles, school enrollment, staff transfers, and payroll obligations on the same date every spring.

For foreign business owners, this April start date affects more than your tax filing deadlines.

It shapes when your Japanese clients have budget to spend, when your staff expect changes to their payslips, when government offices slow down, and when your contracts are up for renewal.

Below, we cover each stage of the fiscal year cycle and what it means in practice for your business.

Why does Japan's fiscal year start in April?

Japan did not always begin its fiscal year in April.

The origin of the April start date traces back to the Meiji era, a period of rapid modernization that lasted from 1868 to 1912.

During the Meiji period, Japan transitioned from a rice-based tax system to cash-based payments.

Prior to this shift, taxes were paid in rice, harvested in the autumn and settled in winter. The new fiscal year would then begin in spring. This agricultural rhythm created a natural alignment with April as the start of a new financial cycle.

A second, more administrative reason came in 1886.

The Japanese government was facing significant fiscal strain and moved the start of the fiscal year from July to April.

By shortening the 1885 fiscal period to just nine months, the government intentionally reduced the period over which it was required to spend, cutting expenditure and easing financial pressure.

Schools, government departments, and companies subsequently aligned their own calendars with the government's April start, and the practice became the established norm.

In 1873, Japan adopted the Gregorian calendar, replacing the traditional lunisolar calendar. However, unlike most countries that also adopted a January-to-December fiscal year at the same time, Japan retained April as the beginning of its business year.

Today, Japan remains one of the few countries where schools, corporations, and government organizations all begin their new year on the same date: April 1.

Japan's fiscal year vs. the calendar year: What is the difference?

Japan uses two distinct annual cycles that do not align:

Cycle |

Start Date |

End Date |

Used By |

|---|---|---|---|

Fiscal year (会計年度) |

April 1 |

March 31 |

Government, schools, most Japanese companies |

Calendar year / Tax year |

January 1 |

December 31 |

Individual income tax, residence tax assessment |

Corporate fiscal year |

Flexible |

Flexible (last day of any chosen month) |

Foreign subsidiaries and some domestic companies |

The fiscal year governs government budgets, school enrollment, university terms, corporate financial reporting for most domestic companies, and the timing of many business contracts.

The calendar year governs the personal income tax system. In Japan, individual income tax is calculated on income earned from January 1 to December 31, not April to March. Employees receive a withholding tax slip (源泉徴収票, gensen choshu hyo) in January covering income from the prior calendar year.

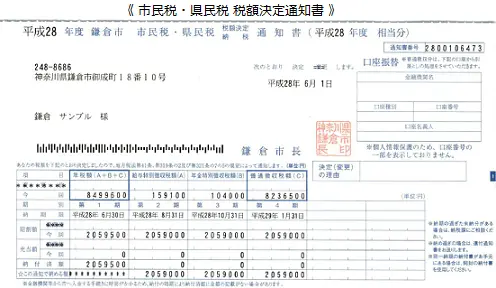

Residence tax (住民税, juminzei) adds a third layer. Local residence tax is assessed on income from the prior calendar year (January to December) but is billed from June of the following year through May. This one-year lag frequently surprises new foreign residents, who pay no residence tax in their first year in Japan but face a full year's bill starting the following June.

Key dates in the Japanese fiscal year calendar

Understanding the fiscal year helps you anticipate the ripple effects on your business's suppliers, staff, lease, clients, and the government offices you depend on.

Here is the full cascade, month by month.

January: The quiet before the storm

January is the calmest month of the Japan fiscal calendar, but three things happen that set the pace for everything that follows.

-

Withholding tax report deadline (January 31). If you employ staff in Japan, you must submit the kyuyo shiharai hokokusho (給与支払報告書, withholding tax report) to your local municipal office by January 31. This covers total employment income paid to each employee during the prior calendar year.

Municipalities use this data to calculate individual residence tax bills, which will arrive with your employees in June.

Fixed asset tax report deadline (January 31). If your company owns depreciable assets in Japan, the fixed asset tax (固定資産税, kotei shisan zei) report is also due on January 31. Fixed asset tax is then payable in four installments across the year, typically in April, July, and two further months that vary by municipality.

Start planning for March. January is the right time to get your year-end accounting, vendor reconciliations, and outstanding invoice reviews in order. By February, your accountant will be busy. By March, everyone will be.

February: Filing season opens

Individual tax return season begins (mid-February). The kakutei shinkoku (確定申告) filing window opens in mid-February and runs to mid-March. This applies to self-employed individuals, freelancers, business owners with personal income to declare, and employees who have side income exceeding ¥200,000 per year.

Corporate tax deadlines for December year-end companies. If your company's fiscal year ends on December 31, your corporate tax returns — covering corporate income tax, inhabitants tax, enterprise tax, and consumption tax — are due at the end of February. This is the first major corporate deadline of the calendar year.

Note for December year-end companies: A one-month filing extension is available for the corporate income tax return, pushing the deadline to the end of March. The extension does not apply to the payment itself, which remains due at the original deadline. Late payment incurs interest at approximately 2.4% per annum for the first two months, rising to 8.7% per annum thereafter.

March: Japan's busiest admin month

March is the month when every major administrative cycle in Japan reaches its deadline simultaneously.

Individual income tax filing deadline (March 15). All kakutei shinkoku filers must submit returns and pay any outstanding income tax by March 15. Missing this date triggers a late filing penalty of 5–15% on unpaid tax, plus interest.

Corporate tax deadlines pile up. Companies with a January 31 fiscal year end face their corporate tax deadlines in late March. For December year-end companies that filed for an extension, the extended filing deadline also falls here.

Consumption tax filing for many businesses. If your company is registered for consumption tax (Japan's 10% VAT equivalent, shohizei), and your fiscal year ended in December, your consumption tax return is due at the end of March. Unlike corporate income tax, consumption tax does not permit filing extensions.

Government offices are at capacity. Every ward office, tax office, and Legal Affairs Bureau across Japan is processing year-end paperwork simultaneously during March. Processing times for applications that are normally quick — address changes, certificate requests, company registration amendments — can slow considerably. If you need anything from a government office before April, submit it in January or February.

Lease renewals and office contract deadlines. Most commercial office leases in Japan run on two-year terms structured around the April fiscal year. Renewal notices typically arrive in January or February for leases expiring in March. If you need to renegotiate terms, request a change of address, or update your registered office address, February is your window. Waiting until March puts you in competition with every other company doing the same thing.

Staff transfers and promotions are announced. Japanese companies announce internal transfers and promotions in March for April implementation. If you work with Japanese corporate clients or suppliers, expect key contacts to change in April. Relationships and introductions need to be refreshed.

April: The tax year resets

April 1 is simultaneously an ending and a beginning. Here's what you can expect:

New fiscal year starts. Budgets reset. New projects are approved. Procurement decisions that were on hold pending budget approval become actionable. If you are chasing a contract with a Japanese corporate client or seeking government procurement work, April is when decision-makers have fresh budget authority.

New graduates begin work. Virtually every large Japanese company onboards its new graduate cohort on April 1. If you are hiring locally, this is the peak of new graduate availability. Mid-career hiring happens year-round, but if you have open roles you planned to fill with new graduates, applications and interviews need to happen in the preceding autumn.

Health insurance and pension rates may adjust. If the government has revised social insurance contribution rates, the new rates take effect in April. Check your payroll calculations at the start of each fiscal year.

Fixed asset tax first installment. The first payment installment on fixed asset tax arrives in April (exact date varies by municipality). Watch your registered business address for the payment notice.

May: Earnings season

For March fiscal year-end companies, May is when annual results are published.

Japanese companies close their March books in April, and most publish their full-year financial results between late April and mid-May. This timing is why Japan's corporate earnings season falls in spring, not in January or February as it does in the US and Europe.

For foreign business owners working with Japanese corporate partners, this timing matters for negotiations, investment decisions, and reading the market.

June: Residence tax

One of the most common financial shocks for foreign business owners and their employees in Japan occurs in June: Residence tax (住民税, or juminzei.)

Japan's residence tax is assessed on the prior calendar year's income and billed from June of the following year, running through May.

The employer collects installments from each employee's monthly salary by special deduction (tokubetsu choshu)—a combined rate of approximately 10% of the prior year's income, covering both prefectural and municipal portions.

Note: Foreign employees who arrived in Japan in 2025 will pay no residence tax in 2025. Starting June 2026, they receive a full year's bill based on their 2025 income. This "year-one free, year-two shock" is predictable if you know about it and a genuine surprise if you do not. Warn new employees before they start.

For foreign business owners paying their own residence tax directly rather than through an employer, the bill arrives from your municipal office in June. Four installment payment options are available if the total exceeds a certain threshold.

August: Interim corporate tax payment

If your company's corporate tax liability for the prior fiscal year exceeded ¥200,000, you are required to make an interim corporate tax payment.

For March fiscal year-end companies, this deadline falls in September. For December fiscal year-end companies, it falls in August.

This is not optional and is not a penalty — it is Japan's estimated tax system.

The interim payment is calculated as half the prior year's tax liability. Missing it triggers late payment interest.

November and December: Year-end adjustment

Nenmatsu chosei (年末調整), the year-end tax adjustment, runs through November and December. Employers reconcile each employee's withheld income tax against their actual annual liability.

Overpaid tax is refunded through the December or January salary; underpaid tax is collected the same way.

As an employer, you are responsible for initiating and completing this process for your staff. Your HR or accounting team will distribute forms in November and must complete the adjustment before the last salary payment in December.

Employees covered by nenmatsu chosei do not need to file a personal income tax return unless they have additional income, which brings the cycle back to February's kakutei shinkoku window.

Can foreign companies choose a different fiscal year?

Yes. Unlike the government fiscal year, which is fixed at April to March, Japanese corporate law permits companies to choose any consecutive 12-month period as their fiscal year.

The fiscal year end must fall on the last day of a calendar month.

In practice, foreign subsidiaries of overseas companies frequently align their Japan fiscal year with their parent company's fiscal calendar.

For example, a US-headquartered company with a December 31 year end will often set its Japanese subsidiary's fiscal year to the same date to simplify consolidated financial reporting. A UK-based company ending its fiscal year in September may do the same.

This flexibility matters because Japan's corporate tax deadlines are calculated relative to a company's own fiscal year end, not the government's. A subsidiary with a December fiscal year-end faces tax filing deadlines at the end of February, not in May.

A Japan branch of a foreign corporation, however, does not have the same flexibility. A branch must use the same accounting period as the corporation in its home country.

Tips for new companies (first year planning)

If you are registering a new company in Japan, choose your fiscal year before incorporation and confirm it in your articles of incorporation (定款, teikan). Changing it later requires amending the articles and notifying the tax office, which adds administrative work and may result in a first fiscal year shorter than 12 months.

Timing tip: Avoid registering in February or March if you can help it. Legal Affairs Bureaus across Japan process company registrations, and standard processing time is approximately three business days. During the peak pre-fiscal-year period, processing can take longer as bureaus handle a surge of registrations and amendments. January or October are quieter registration windows.

How MailMate helps you stay on top of Japan's fiscal year

Every tax notice, government filing, and invoice demand in Japan arrives by post. During March and April, that volume peaks. For foreign business owners without dedicated admin staff, this is where deadlines get missed and penalties accumulate.

MailMate is the only bilingual mail management platform built specifically for foreign businesses in Japan. It handles every layer of the paperwork problem so you do not have to.

Virtual Mailbox. Your company mail is received at a registered Tokyo or Fukuoka address, scanned, and delivered to your team dashboard as a searchable PDF with automatic English translation. Share directly with your accountant, pay bills in-app, and access your full mail history from anywhere in the world.

Send Mail from Japan. Responding to a tax office notice or filing a corporate registration amendment requires physical mail in Japan. Upload your document, choose a carrier, and MailMate posts it on your behalf. Deadline, tracking status, and delivery confirmation are all visible in your dashboard. No post office visits required.

AP Automation. Japanese vendors still send paper invoices. Tracking them alongside digital ones, entering data manually, and reconciling everything before your fiscal year end costs your team hours they do not have. MailMate captures all invoices in one place, extracts the data automatically, and flags duplicates before they create problems. Your accountant gets a clean report. You close the books on time.

When the fiscal year-end deadline cascade hits in March, MailMate customers are already ahead of it.

Frequently Asked Questions

What is Japan's fiscal year?

Japan's fiscal year runs from April 1 to March 31 of the following year. This period is used by the national government, most Japanese companies, public schools, and universities for financial reporting, budgeting, and tax purposes. It is referred to in Japanese as kaikei nendo (会計年度).

Why does Japan's fiscal year start in April?

Japan's April fiscal year start has roots in the Meiji era. Tax collection historically followed the agricultural cycle, with rice taxes paid in winter after the autumn harvest and a new fiscal period beginning in spring. An 1886 government budget reform moved the fiscal start date from July to April, and schools and companies followed. The April start has been standard practice ever since.

Is Japan's fiscal year the same as the tax year for individuals?

No. Japan's individual income tax is based on the calendar year, from January 1 to December 31. The April-to-March fiscal year applies to government budgets and most corporate financial reporting. Residence tax is also based on the calendar year income, but is billed from June of the following year.

Can a foreign company in Japan choose a different fiscal year?

Yes. Japanese law permits corporations to choose any 12-month period as their fiscal year, provided the year end falls on the last day of a month. Foreign subsidiaries frequently align with their parent company's fiscal calendar, for example December 31 for US-headquartered companies. A Japan branch of a foreign corporation must use the same fiscal year as the head office.

When are corporate tax returns due in Japan?

Corporate tax returns are due within two months of the company's fiscal year end. For a company with a March 31 year end, this means the end of May. For a company with a December 31 year end, this means the end of February. A one-month filing extension is available for corporate income tax, but this does not extend the payment deadline.

What is nenmatsu chosei and when does it happen?

Nenmatsu chosei (年末調整) is Japan's year-end tax adjustment, carried out by employers in November and December. It reconciles the income tax withheld from each employee's monthly salary throughout the calendar year against their actual tax liability. Overpayments are refunded through the December or January salary. Most salaried employees do not need to file a personal tax return after the adjustment is completed.

What is the residence tax timing lag in Japan?

Residence tax (juminzei) is assessed on income earned in the prior calendar year and is billed beginning in June of the following year. This means new arrivals in Japan pay no residence tax for the first months or year, then receive a full annual bill the following June. Employees pay in monthly installments from June through May, deducted from their salary by their employer.

What happens to corporate tax deadlines if a company changes its fiscal year?

Changing a company's fiscal year in Japan requires a formal amendment to the articles of incorporation and notification to the relevant tax office. The first fiscal period after the change may be shorter than 12 months. Tax deadlines recalculate from the new fiscal year end date. A tax accountant should handle this process to avoid missed filings or incorrect payment dates.

In closing

Japan's April fiscal year is not just an accounting convention. It sets the rhythm for how businesses hire, budget, contract, and communicate across the entire country. Once you understand the cycle, the pressure points become predictable — and predictable problems are manageable ones.

The practical takeaways: file early, plan cash flow around tax payment months, choose your fiscal year end before you incorporate, and do not assume your Japanese contacts will be in the same role come April. If your business generates physical mail in Japan and you are not on top of it during March and April, that is the highest-risk period for missed deadlines.

If you have questions about managing Japanese paperwork or need a registered business address in Japan, MailMate's team is available to help.

Spending too long figuring out your Japanese mail?

Virtual mail + translation services start at 3800 per month. 30-day money-back guarantee.